DEAL WITH DEBT

“Annual income twenty pounds, annual expenditure nineteen [pounds] nineteen [shillings] and six [pence], result happiness. Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery.”

Charles Dickens, David Copperfield

Waking up on Monday morning with that ache in the pit of your stomach – that feeling you have before – when you’ve broken a window, shaved the dog or thumped your sister a bit too hard – just before mum or dad arrive home, it starts. It’s a primal nag in the stomach, the fear of the unknown – what is going to happen, what are they going to say. Or worse still, do?

Being in debt, to the point of monthly income less debt repayments means you won’t have enough, won’t be able to meet the costs of food or council tax this month is when that feeling starts – it’s the same fear.

That “oh ffin’ shit” feeling that just won’t go away, no matter how much [insert drug of choice here] you consume – it stays inside making your stomach feel like John Hurt just before the birth in Alien when he has his stomach exploded by the monster. Being in debt, not having enough to meet your obligations is just like that. It’s probably caused by the stress hormone cortisol shutting down your stomach because it’s not going to waste energy you’ll need for running away – digestion can wait.

Only you can’t run. This problem is yours, bills are coming fast, cancelling the direct debit means you’ll soon be getting phone calls and the stress levels are fast increasing – the knot in the stomach is now just below crippling – getting up and going to work is becoming hard and maintaining relationships is difficult, because your whole thinking, the only voice you can hear is asking questions – what are you going to do?

Debt that is out of control is more stressful than divorce, moving house, having a child and major surgery all at the same time. It’s a documented cause of more health problems than just about anything else. Depression, anxiety and suicide – are all higher than average for people with serious debt. It’s estimated that over 100,000 people per year attempt suicide because of debt and 420,000 have fought about it. Time to get a handle on that.

“Suicide is a permanent solution to a temporary problem.”

Dr Dylan Keogh BBC1’s Casualty.

Important Supporting Information

Debt Is Everywhere

Current UK National Debt – the amount owed by the government is £2.199 trillion (at May 2016). At the end of February 2019 personal debt – the amount owed by us all personally was £1.63 trillion. Just so you know: a trillion seconds = 31,688 years or would take to back to 29,000 years bc.

Jesus was just a twinkle in an eye somewhere.

There is something about debt, on one level it seems we can’t live without it, yet millions do manage it. Supported by the government and the banks we are encouraged to live now, buy now, have it all now on borrowed money – effectively mortgaging your future very nicely.

Borrow if you need, just understand how bad it can be for your financial health – like smoking it feels good at the time, but stuck in a cancer ward with terminal lung cancer does not seem that great.

The message we get from all of those trying to sell us things is this …Imagine how good you’ll feel when you have x or y. Just do it! There are many problems with this kind of thinking or approach to having stuff, and most of the stuff we all buy on credit is just stuff; first problem is this.

It’s a poor man’s (or woman’s) approach to life. The wealthy understand the truth about borrowing – you mortgage your future income in order to get that car or holiday this week rather than next month or next year, waiting for the right time, perhaps when you have saved enough.

Wealthy people, those that are able to earn and keep hold of money have very different spending patterns to most of us, and certainly don’t borrow to buy stuff. Working on your buying decisions is one way to ensure you become FI (financial independent) at some time in your life.

Long after the buzz of the purchase has gone, you will still be paying for it out of your future income.

As a ‘for example’ I want to show you something that will fundamentally change how you think about debt. Importantly it should make you think more seriously about the debt you have any what to do about it.

One of my oldest clients, Bob, owned a great business. Even during the 2008 crisis it was going well, he was great at his job and had managed to bring his business round despite it struggling whilst his dad was alive. No matter what happened – cash continued to come in. Helped it was niche business in a sector most of us have no idea about. In fact it was the perfect model. Few staff, little overhead and a niche product. Just great.

Because of the amount of cash and profits in the business, Bob was constantly being sold loans, credit cards. Finance of all sorts. Both him and his wife were driving top dollar German sports cars, along with a couple of expensive horses and ballet lessons for the little’un. Whenever cash got a little low, the bank would pop up and drop in a bit of finance, factor a few invoices – then expansion got the better of Bob.

Some crowdfunding dropped in another quarter of a mill, didn’t matter the business was soaking it up – no problem. Life was really rosy, weekends in Paris, three week holidays with all of the kids and their friends. Overseas property – it was all coming together quite nicely – life was fucking sweet – 2009,10, 11, 12 and 13 – into 14 and 15,16 and 17 life was just the best.

In the background was a shitstorm brewing nicely. The accountant was only interested in making sure his fee’s were increasing well above inflation. He was now doing payroll, VAT along with managing some parts of HR and generally getting involved to the tune of around £1500 per month (plus VAT of course) and still not interested in having a reasonable conversation with Bob about the level of unsecured borrowing now attached to the business nor the amount that was being spent on the business debit card – bottle of Bollinger on a Sunday at Ascot (£190) and Ballet Fee’s at £400 a month.

The lenders kept piling up the debt, few questions asked. Until the point where Bob realised that the £35k a month turnover was all being soaked up. Loans and bullet repayments along with the company credit card, leases on the pair of Germans and a few bottles of bubbly – were taking their toll. Now some £10k per month was being demanded in repayments, but that was OK as another line of credit was sourced by a family member – another idiot that didn’t really have a clue. This time a secured loan was arranged on equipment – £10k wouldn’t even touch the sides in this massive bucket of debt the business was in. But at least the Germans could stay for another month.

The accountant wasn’t even getting nervous. See Bob like a lot of other business owners think that the ‘specialist adviser’ to the business would know what’s going on – they did the money stuff – surely, Bob thought to himself – the accountant would have been in touch if there was a problem. Problem with that is this – the total monthly income for the business was now being sucked dry by those who’d lent the money – quite rightly as well. You borrow money the lender expects it back – only now the borrowing – and the excess spending was in danger of destroying the company. Just a quick glance at the maths shows how this worked against Bob.

Company Barclaycard

This calculation makes a couple of assumptions.

Balance £18.5k Interest Rate 21.9%. The total charge £30 and the total paid £49k. In this instance the lender turns £18.500 into £49k over the repayment period.

Bob, had four of these.

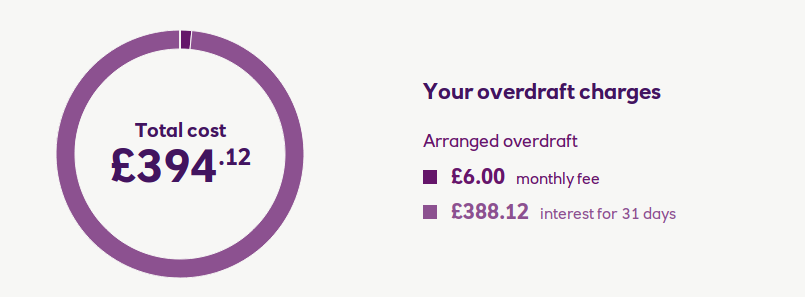

The overdraft was also interesting, Bob was in a bad way with this. £60k at least. Using the Natwest calculator you’ll see that in interest alone [for £25k overdrawn] his charges would have been £388 per month more than double that and his overdraft charges alone would have been in region of £850 per month.

Debt was the obvious cause of Bob’s problems but what he was not aware of was this. The situation he found himself in had crept up and was about to bit him hard. Just to service some of the debt – was taking up about a third of his profit, and that was without his other loan and the payments for the German.

Just think about this for a short moment, Bob’s business was struggling. Despite being profitable and able to run itself because Bob had been stupid – he’d taken his eye of the ball, overspent by a few quid over a few years and the whole thing was now going to bite his bum.

Stress, his wife left him, he went into a bit of

Now this story is no unusual. Bob is going on all over the world. Sure, he should have seen it coming – but have you? Do you know how much debt your business has, do you know what the servicing costs are? Do you know how to manage it more effectively do you know how to turn it around so it works for you?

Far too many businesses owners don’t. Which I why I spend my time working with small firms that want to get this area of their planning sorted, and sorted correctly. Before it bites you on the bum.

How Profitable Are Credit Card Companies?

Credit card lenders are some of the most profitable firms on the planet. How else would the likes of Barclays be able to pay a fine of £2.1bn and to also ‘write off’ billions of pounds in bad debt and still make a profit? Answers to that one on a postcard please.

Sure you need an office, staff and a little infrastructure. It also helps if you have a fractional banking system to support the organisation. But actually it’s a very simple business, no stock – any money you need for lending is created electronically and once you have a few systems in place, once the legal team can run circles around the regulations you are in business.

Of course, not everyone pays the bills on time or at all. But this is priced in. All of the card providers can work out roughly how much bad debt they are likely to have and price things accordingly.

Fact is lending money at 18% plus interest every year is a very profitable business. You can borrow money, as a bank from the open markets at a very low rate – lets assume 1.5% pa interest, you lend that money 16.5% profit. Of course some people pay their credit cards in full at the end of the month. Not good for the credit card company – in order to cover the costs of that you can charge the retailer a couple of points for processing the card, that cost of course is already priced into the transaction [the customer always pays].

Either way it a no lose situation for card company. Of course there is the issue of bad debt – not every customer pays on time or at all. Credit card companies are so profitable they can afford to write of £1.4bn in December of last year alone. If one pound was one second then 1.4bn seconds is around 44 years. Despite this massive write off the card companies still remain in business and still remain profitable.

They are hoovering up lives, hoovering up your future earnings. It’s the perfect form of capitalism, just the best business to be in.

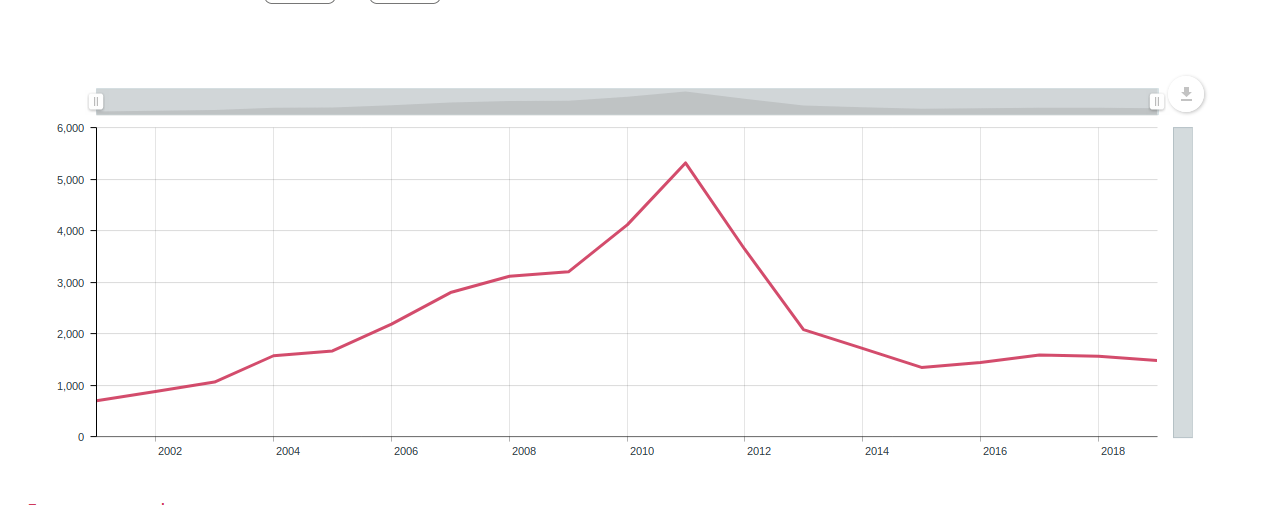

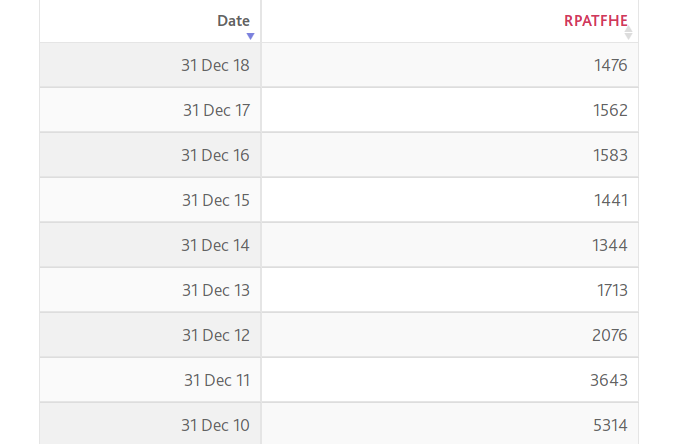

Bank of England Stats

Source – Bank of England

Debt Truths

There are a lot of mistruths around debt both for business owners and individuals.

Sure some debt can “bite you on the bum” quite hard. Most debts or non payment of debts won’t mean you end up in prison. Inland Revenue, Council Tax are exemptions to this rule.

Credit Card Debt

Rarely enforced by the courts as little court action is used. After three months debts are normally sold on to a debt collector for around 20p in the £ and that’s it.

Overdrafts

Roughly the same, some banks hang on a for bit longer.

Secured Loans

Especially if it’s your main home – be careful. Priority debt.

Mortgages/Rent

Priority debt, court action is required but possession can and is granted.

Car Loans – Leases

Normally they’d be trying to get your car back after three months of missed payments

No exhaustive lists here but nearly all debts will fall into one or more of these.

If you are a business owner and have any of these get in touch today (link below)

Repay/Overpay

I have a budget planner available from my website (email me on admin@therichardsmith.com and ask me for a copy of it.

On the debt side of this planner I ask you to rank debt in order of it’s interest charge. Often you will find that the actual interest charge on much of your debt varies from 16% – 28% right down as low as 1% for mortgages.

You should then consider what borrowing can be repaid without penalty – credit cards are not normally a problem, but loans and other types of finance may have a penalty, check first.

Once you know what the most expensive debt is you should start to make larger payments to this, and maintain the minimum or contracted payment to the rest of your debt.

This method provides you with a ‘snowball effect’ as the more expensive debt starts to reduce, thus you’ll be paying less interest and more capital; forcing the debt to reduce.

True Cost Of Credit – Alison Average.

A few years ago Alison went on a very nice holiday and she put the cost of this on her credit card which leaves her with just half of the UK average debt of £4500.

This is likely to be paid off over the next ten years or so if she doesn’t spend any more on her card. Based on average repayment time, and an interest rate of 18.9% assuming she makes the minimum payment she should clear the balance completely in around 31 years, and pay £6350 in interest. Total cost is over ten grand.